Yrefy, LLC is a U.S.-based specialty finance company that focuses on an unusual corner of lending: the refinancing of distressed or defaulted private student loans. finlocity.com

Here’s a quick summary of the business model and background:

Founded in 2017 (per Finlocity) with a mission to assist borrowers burdened by delinquent or defaulted private student-loan debt.

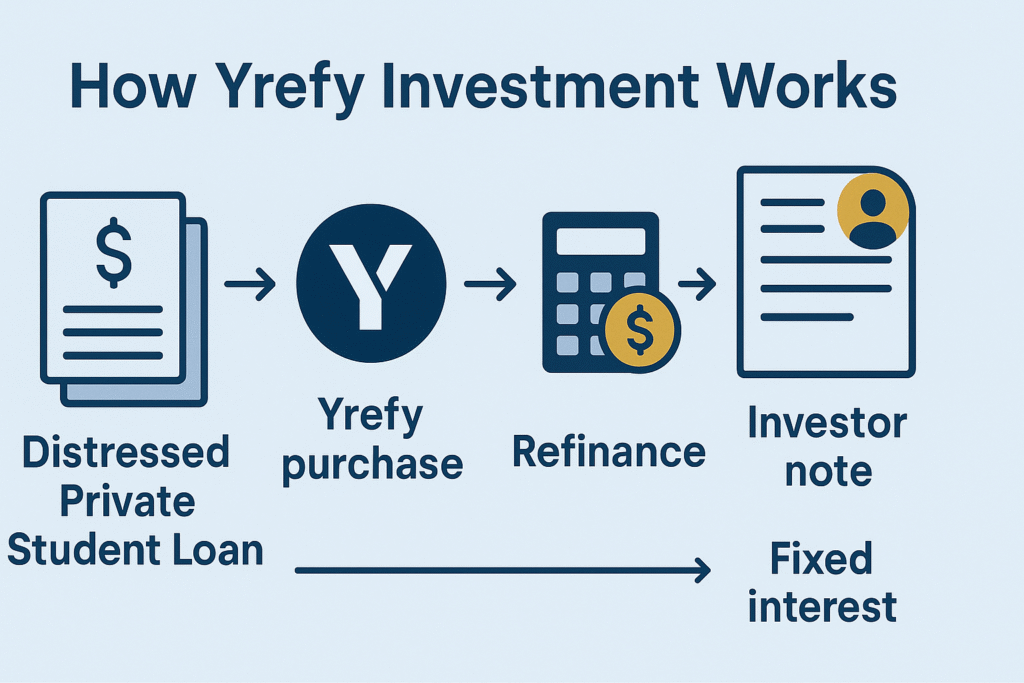

Its core strategy: buy or negotiate distressed private student-loan portfolios (often at steep discounts), refinance them into newer loans with fixed rates, then service the loans and manage repayments.

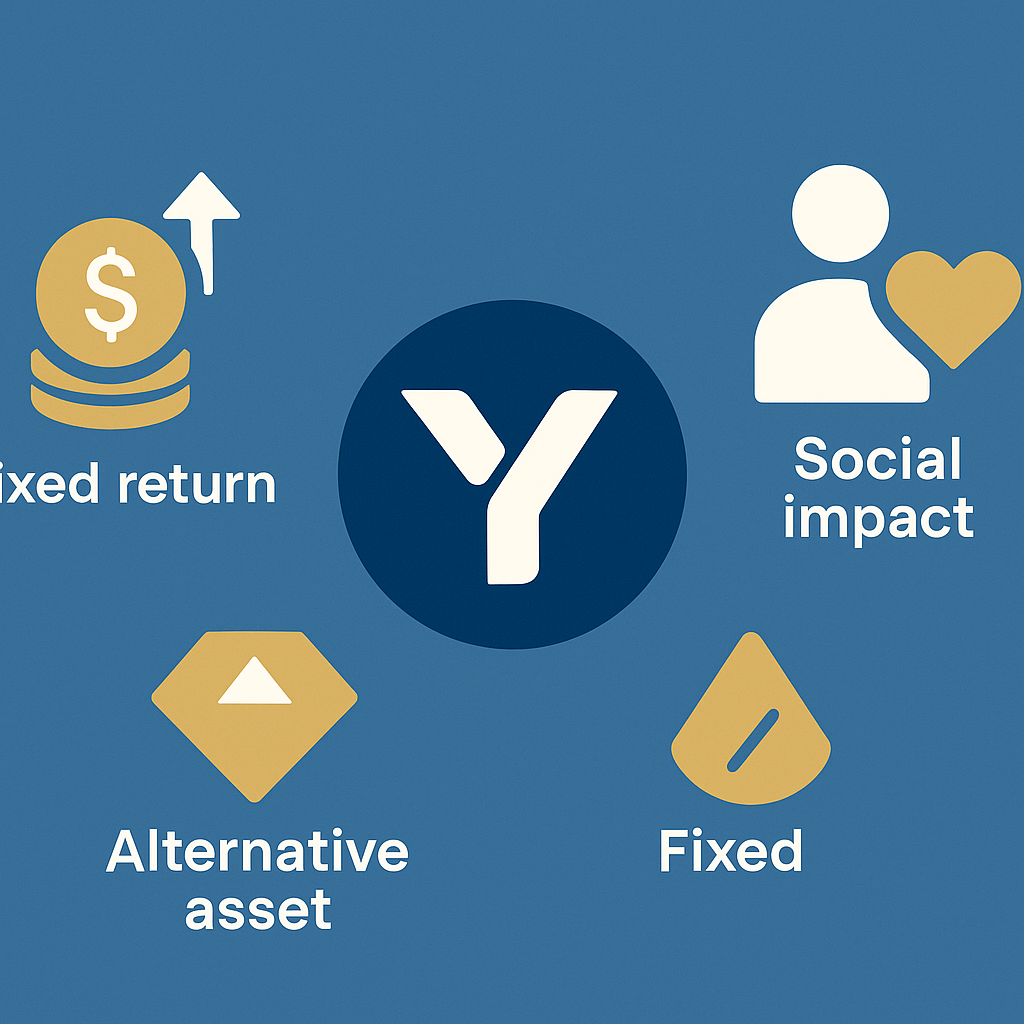

On the investor side, Yrefy offers promissory-note private placements under Regulation D (506(c)) for accredited investors only. These promissory notes are backed by the portfolio of refinanced loans. InvestorPage

According to Yrefy’s investor-site, the minimum investment is US$50,000, and available terms range from 12 to 60 months with fixed rates (e.g., up to 10.25% annual for a 60-month class) based on class choice. InvestorPage

So when you talk about “Yrefy investment” you are generally referring to investing in Yrefy’s promissory-notes tied to their private student-loan refinancing business. The investment takes the form of fixed-term notes offered to accredited investors, not publicly traded securities.

Related Read: If you’re planning to buy gold for investment, read out guide on 10 Reasons to Invest in Gold.

Related Read: If you’re planning to buy gold for investment, read out guide on 10 Reasons to Invest in Gold.

Leave a Reply