Introduction to In House Financing

When it comes to making big purchases like cars, homes, or even furniture, finding the right way to pay is often stressful. While many people immediately think of banks or credit unions, there’s another option worth considering: in house financing.

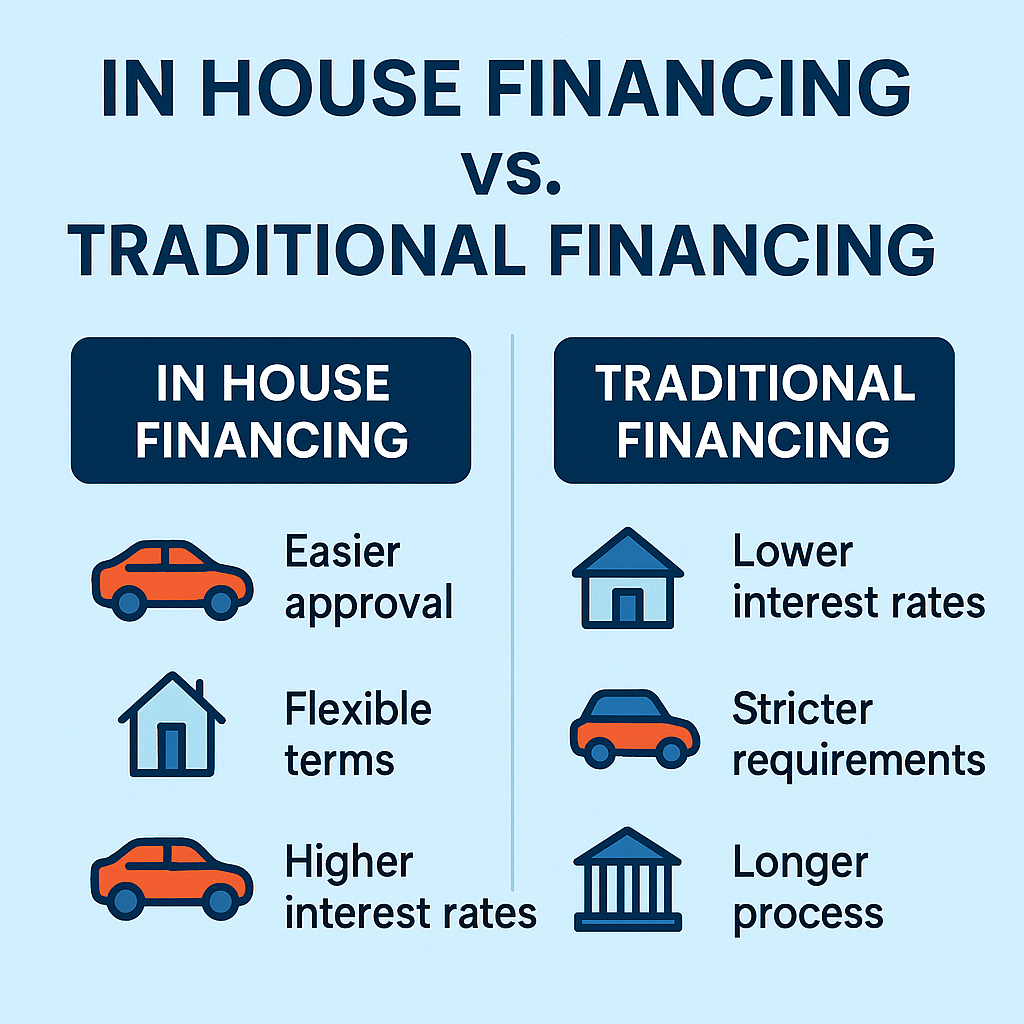

With in house financing, the seller provides the loan directly instead of sending you to a third-party lender. This makes the process faster, more convenient, and sometimes more flexible for buyers with limited credit. However, while it offers easier approvals, it also comes with higher interest rates and stricter terms.

In this guide, we’ll explore everything you need to know about it in 2025—how it works, its pros and cons, and practical tips to use it wisely. We’ll also compare it with traditional financing so you can make an informed decision that fits your financial goals.

👉 According to Investopedia’s guide on In-House Financing, this type of loan has grown in popularity in sectors like auto sales and real estate, especially for borrowers with weaker credit histories.

What Is In House Financing?

it means the business selling a product also provides the loan for purchasing it. Instead of applying at a traditional bank, you sign a loan agreement directly with the dealer, store, or service provider.

Common examples include:

Car dealerships offering buy-here-pay-here loans

Furniture stores with monthly installment plans

Dental offices with treatment financing plans

Real estate developers offering seller financing

How Does In House Financing Work?

Application Process – Customers apply directly through the seller.

Approval Criteria – Requirements may be less strict than banks, making it accessible to those with lower credit scores.

Payment Terms – Payments are made directly to the business, often weekly or monthly.

Interest Rates – May be higher compared to traditional bank loans.

Advantages of In House Financing

Convenience – Faster approvals without third-party involvement.

Flexible Credit Requirements – Easier for buyers with poor or no credit.

One-Stop Shop – You buy and finance in the same place.

Build Credit – Some businesses report payments to credit bureaus.

Drawbacks of In House Financing

Higher Interest Rates – Riskier borrowers often pay more.

Limited Negotiation – Terms are set by the seller.

Repossession Risk – Dealers may repossess quickly if you miss payments.

Smaller Loan Amounts – Often limited compared to traditional banks.

In House Financing vs. Traditional Financing

| Feature | Financing | Traditional Bank Loan |

|---|---|---|

Approval Speed | Fast | Slower (requires review) |

Credit Requirements | Flexible | Stricter |

Interest Rates | Higher | Lower (for good credit) |

Payment Location | Direct to Seller | Bank/credit union |

When Should You Consider it?

If your credit score is low and banks won’t approve you

When you need fast approval for an urgent purchase

If you prefer convenience and direct payment to the seller

Tips

Always compare interest rates with traditional lenders.

Read the contract carefully for hidden fees.

Ensure payments fit your monthly budget.

Consider refinancing later if your credit improves.

👉 For better long-term planning, learn how to Calculate HELOC Payment Easily to manage bigger financial commitments.

FAQs

Q1: Is in house financing a good idea?

It depends on your credit situation. It can be helpful if traditional financing isn’t an option, but interest rates are often higher.

Q2: Does in house financing affect my credit score?

Yes, if the business reports to credit bureaus. Otherwise, it won’t build your credit history.

Q3: Can I negotiate terms in in house financing?

Sometimes, but sellers usually set strict terms.

Q4: What types of businesses offer in house financing?

Car dealerships, furniture stores, medical offices, and real estate developers.

Q5: Can I refinance later?

Yes, if your credit improves, refinancing with a traditional lender could lower your payments.

Conclusion

In house financing can be a lifesaver for those who need quick approval or have limited credit options. However, it’s crucial to weigh the pros and cons, compare it with traditional loans, and ensure the payment plan fits your budget.

By making smart financial choices and using tools like budgeting apps and investment calculators, you can set yourself up for long-term success.

👉 Want to dive deeper into smart money tools? Check out our article on the Dave Ramsey Investment Calculator to learn how compound growth can transform your savings.

Leave a Reply